Interesting proposal from David Stockman, Reagan's OMB head from 1981 to 1985: "One way to reverse this dangerous and unstable deformation of policy would be to return to the vision of Carter Glass, and employ the Fed as a 'banker’s bank.' In such a situation, the Fed takes its cues from the market. The market sets prices (i.e., interest rates on money and debt), and the Fed only provides additional liquidity, in exchange for sound collateral, at a penalty rate, when the banks needed liquidity." His book appears to be a pretty good read, too.

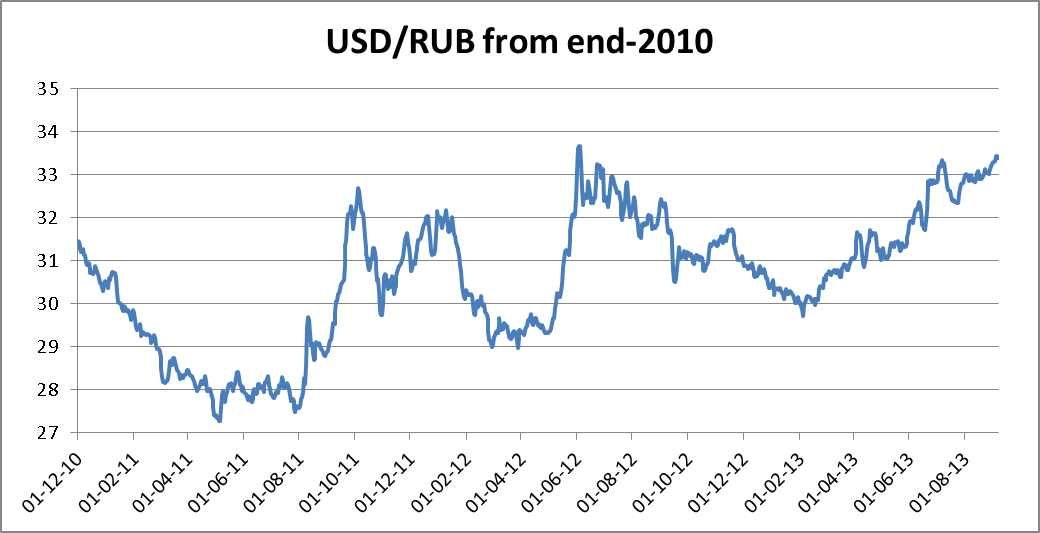

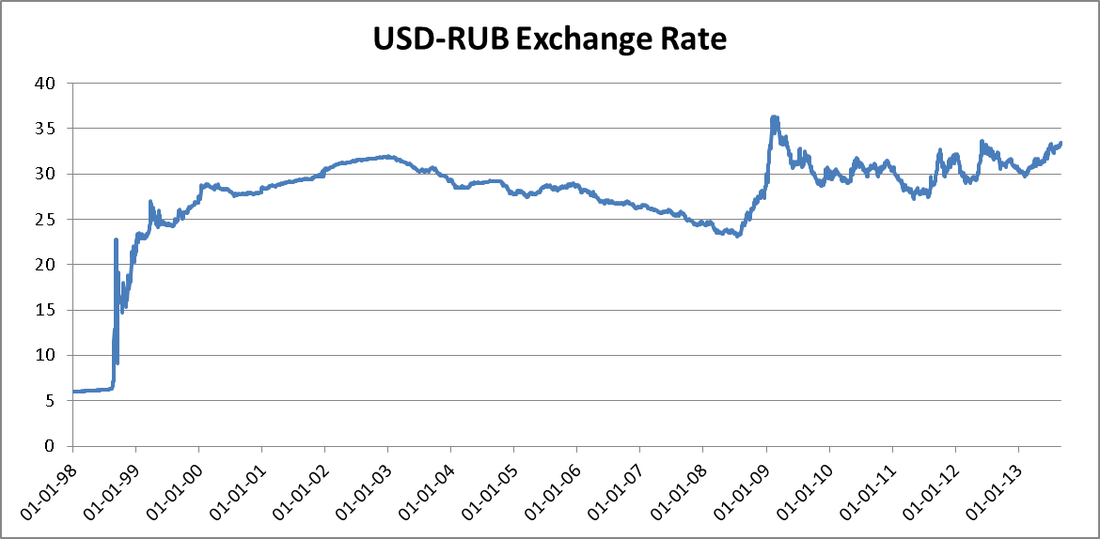

With apologies to Foxy Shazam With apologies to Foxy Shazam Living in Russia, working for an emerging markets think tank, and being paid in rubles, makes you acutely aware of geopolitical tensions, emerging market ripples, and Russia-specific factors. This has been especially true over the summer as, to be polite about it, the ruble plummeted against the US dollar. Now, there's usually a good amount of seasonality for the ruble/USD exchange rate, with drops in the summer due to the lower price of oil and, of course, the fact that the Russians book it out of Moscow as fast as their private jets will take them (meaning more demand for foreign currencies and less for rubles). But this summer, the bottom dropped out:  From just about the 29.8 mark in February, the ruble is now at about 33.40 and climbing daily (with bank premia for foreign exchange, you can sell ruble at about 33.85 this morning with Raiffeisen). That's a loss of 12% (hellooooo depreciated paycheck), not gigantic by historical standards but still a pretty hefty drop in a market where the price of oil hasn't seen major swings. But is this an aberration? Well, yes and no - looking at the Ruble since it became "new" in 1998, we're basically part of a trend that started during the global financial crisis and shows no signs of abating:  So we're not as weak as we were, not as strong as we were, just somewhat bouncing around in the 30-35 range. And this is in line with a general sell-off from emerging markets, as the financial world starts to believe that Ben Bernanke's money spigot won't run forever and "quantitative easing" might actually recede from the US. Russia is just part of a general trend of emerging market pullback.

That's the no, this is not an aberration. But the yes is that, for some reason, the world seems to be waking up to the unsustainable nature of Putin's economy, and we have a big shift in momentum just over the past two months. Putin hasn't helped any, as his new Central Bank head is fairly similar to those in Western countries; i.e. looser monetary policy somehow grows economies magically! And Russia has always been willing to use its economic riches for geopolitical gain (although, as a colleague of mine detailed in RBK Daily earlier this year, the Russian stance on Syria actually caused it some problems with the Saudis, who retaliated by ramping up their oil production to depress prices). The question is, can the almost completely un-diversified Russian economy survive the next round of economic uncertainty? The best part of this is also the bit that makes me so angry - the structure of the Russian economy has been basically frozen in place during Putin's reign, due to uncertain property rights, bureaucratic nightmares (one need only look at Russia's place in Doing Business), and a widespread perception of corruption. And, of course, the institutions needed for a market economy are still fledgling here, subsumed to the formal bureaucratic apparatus of the state. Transaction costs may not have been spawned in Russia, but by golly this place perfected them. So why are traders and the world starting to fret now about Russia? Why is the ruble sliding now? Why have Russia's revised growth estimates suddenly taken the world by storm? Better renegotiate my contract, because I sense that 34-35 rubles to the dollar isn't far off. As noted in my earlier post on the Taylor rule paper, the head of a Central Bank can do a LOT of damage. Which is why I am surprised that the Economist is full-throated in favour of Janet Yellen as the next Head of the Fed. The biggest plus seems to be that she would be a continuation of Bernanke's tenure, albeit a bit more diplomatic. Indeed, even some of my fellow libertarian-inflected colleagues at my former employer (Reason) seem to be fairly on-board with Dr. Yellen, seeing her also as a pragmatist.

I'm not convinced (along with Robert Murphy, the Wall Street Journal, and others) - if anything, the fact that Yellen would be a continuation of Helicopter Ben's policies should automatically raise suspicion. She is already on record as part of the "a little inflation now and then is a good thing" school, which would in and of itself be problematic... but is even worse with a Fed actively stoking the fires of hyperinflation and basing its policy decisions on perhaps the wrong metrics. In fact, as noted in this article, "I think it’s a fair reading of a typical Janet Yellen speech that she’s more concerned about high unemployment.” This is precisely the central bank mentality that led to stagflation of the 1970s. Besides, anyone who Joseph Stiglitz likes already has two strikes against them. A new study by Alex Nikolsko-Rzhevskyy, David H. Papell , and Ruxandra Prodan takes a very interesting look at the monetary policy regimes in the US over the past 40 years, looking for deviations from the Taylor rule. By itself, this isn't great news - John B. Taylor (whom I used to work with at Treasury) has been trumpeting the myriad of deviations from his rule for years now. However, the paper uses rigorous econometric methods (including a Markov switching model) to extrapolate the regime that monetary policy operated under: high deviations are indicative of a discretionary regime, while low deviations can be characterized as (Taylor) rules-based.

The great leap forward that this paper establishes is that yes Virginia, indeed the Fed went off the rails from 2001 onward (and, as many Austrians correctly suggest, was the major force behind the Great Financial Crisis), much as it was off the rails in terms of discretion from 1974-1985. I wonder what characterized both of those eras? Well, in the 1970s, of course, it was stagflation (which Keynesians still can't account for and which smashes the incidental correlations of the "Phillips Curve" to bits), while in the naughties it was over- (mal-) investment. So there wasn't exactly the same effect during the Fed's discretionary period, but this can also be attributed to the fact that the international economic world was different in the 1970s (protectionist, closed, far less integrated) than the 2000s were. However, on the flip side, the boom of the 1980s and the 1990s appeared to be the real deal. More sustainable and not affected due to the Fed, mainly due to the lack of Fed volatility... and we all know how damaging policy volatility can be. The authors don't explore these corollary effects (they've really done enough with their econometrics), but it's an interesting area for future research. And of course, the institutional angle on this is similar to what I explored in my Banks and Bank Systems paper last year - the institutional make-up of a Central Bank may matter less than the institutional goal of the Bank, or rather, what the inherent nature of the institution is (as someone mentioned earlier this year, an institution where you need to have a great leader not to screw up the economy is by definition not a good institution). To put it simply, Central Banks wield great power and abilities to muck up an economy, and the only way to minimize this may be via the proper policies - which, in this case, seems to be adhering to a rules-based mechanism rather than going at it willy-nilly. |

AuthorDr. Christopher Hartwell is an institutional economist and President of CASE Warsaw. All commentary on this page is exclusively his own and in no way represents the views of CASE, his wife, his dog, or anyone else. Especially not his wife or his dog. Archives

July 2014

Categories

All

|

RSS Feed

RSS Feed